How Competitors Use Industrial Automation to Win (And What It Costs You)

Every 1% jump in robot density adds 5.1% productivity. 95% of predictive maintenance adopters see positive ROI. Your competitors know this already.

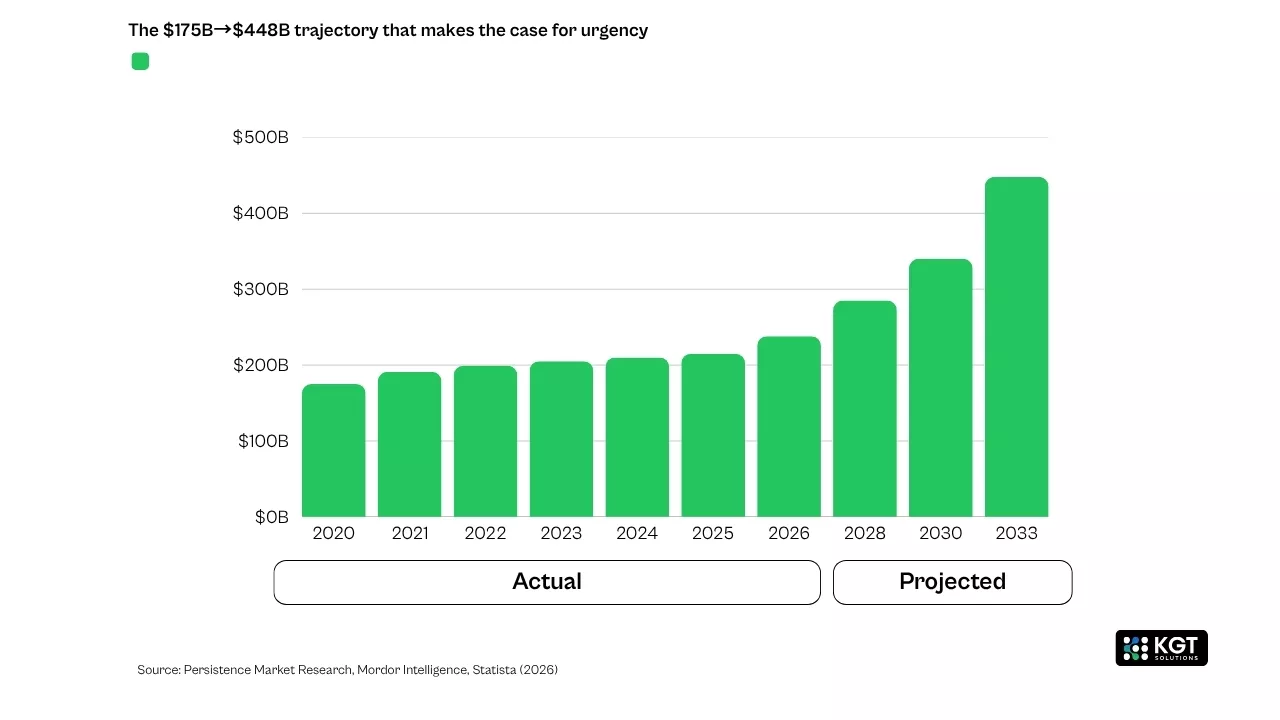

Your competitors are not just cutting costs with industrial automation they are building operational moats that get wider every quarter. The global industrial automation market crossed USD 215 billion in 2025 and is projected to reach USD 448 billion by 2033, growing at a 9.6% CAGR (Persistence Market Research, 2026). That trajectory is not driven by hype. It is driven by companies that have figured out how to turn automation investments into compounding advantages across productivity, quality, maintenance, and speed-to-market.

Industrial automation is the use of control systems, robotics, AI, and IoT-connected devices to operate industrial processes with minimal human intervention, enabling higher efficiency, consistency, and real-time decision-making.

This blog unpacks exactly how forward-thinking manufacturers are weaponizing these technologies - from PLC programming and control systems to digital twins and automated warehouses and what you need to do to stop falling behind.

Why Industrial Automation Is No Longer Optional

Each 1% increase in robot density bumps productivity 5.1%. And 95% of companies doing predictive maintenance say they got positive ROI.

A few years ago, automation was a capital expenditure decision weighed against quarterly budgets. Today, it is a survival question. According to Mordor Intelligence (2026), the market reached USD 238.37 billion in 2026, with Asia-Pacific alone commanding a 43.1% share. Companies that delay adoption are not standing still they are actively losing ground.

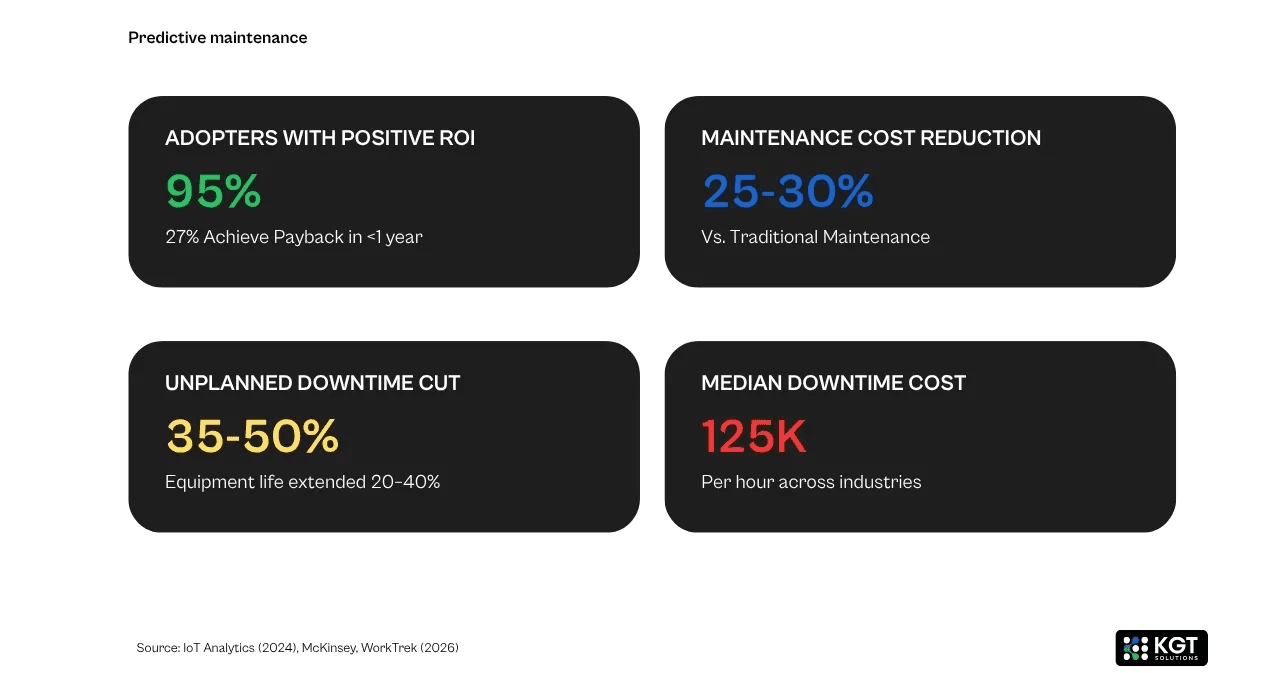

The numbers make this painfully clear. McKinsey estimates that predictive maintenance alone could generate USD 630 billion in annual savings across manufacturing sectors. Meanwhile, 95% of predictive maintenance adopters report positive ROI, and 27% achieve full cost recovery within just one year (IoT Analytics, 2024). Competitors capturing these savings are reinvesting them into further automation, creating a cycle that laggards cannot easily break.

The International Trade Administration reports that for every 1% rise in industrial robot density, productivity increases by 5.1% among the least robot-adopting industries. That is not a marginal gain it is a structural shift in competitive positioning.

How Competitors Deploy Industrial Control Systems for Precision

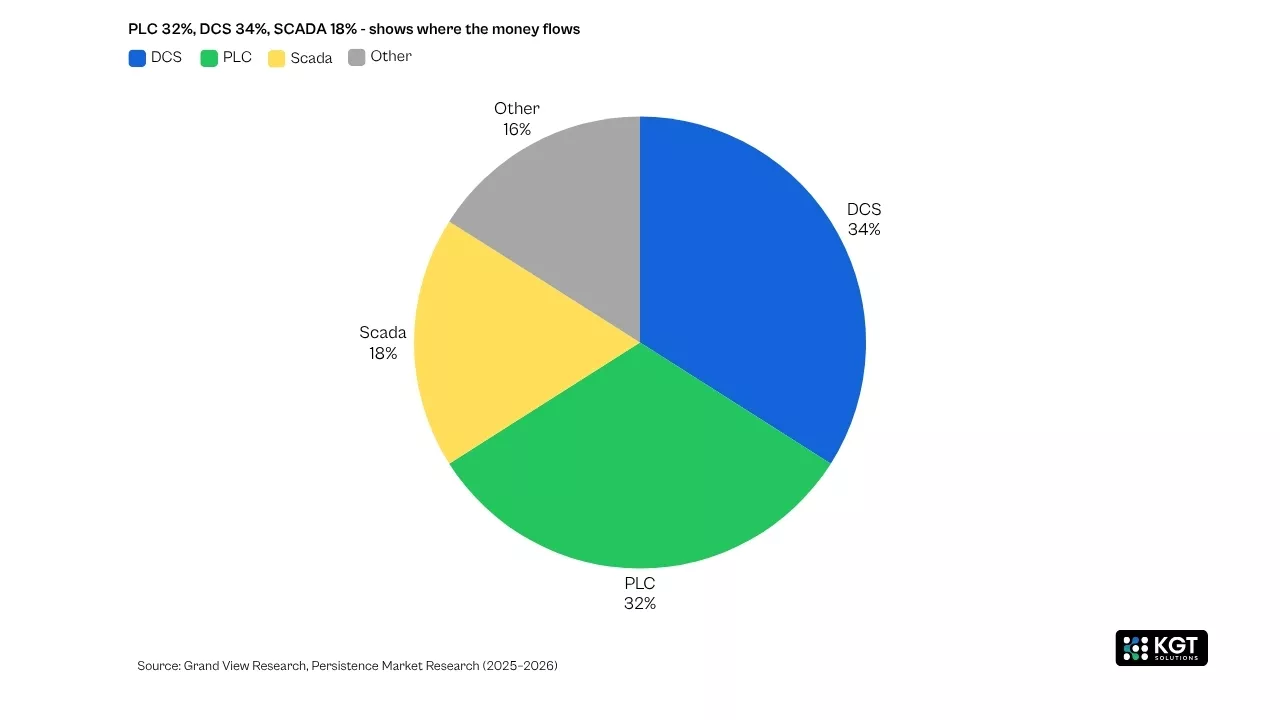

DCS holds 34%+ of the controls market. The companies winning this race unify their PLC, DCS, and SCADA data into a single analytics layer.

Industrial control systems - including PLCs, DCS, and SCADA - form the backbone of every automated manufacturing environment, enabling real-time monitoring, process optimization, and autonomous decision-making.

The distributed control system (DCS) segment alone accounted for over 34% of the automation control systems market in 2025 (Grand View Research). But leading competitors are not merely installing these systems. They are integrating them into unified architectures where every sensor, actuator, and controller feeds into a single operational intelligence layer.

The competitive advantage of industrial control systems lies not in the hardware itself, but in the integration layer companies that unify PLC, DCS, and SCADA data into a single analytics platform make faster, more accurate production decisions than competitors managing siloed systems.

The Role of Automation PLC in Competitive Manufacturing

PLCs make up 32% of automation revenue. Pair them with edge computing and you cut cycle times and labor costs by 25-30%.

Programmable Logic Controllers (PLCs) account for over 32% of market revenue in automation solutions, making PLC industrial automation the single most deployed control technology across both discrete and process manufacturing (Persistence Market Research, 2026). Companies investing in advanced industrial PLC programming are achieving cycle time reductions that directly translate into throughput gains.

Modern automation PLC systems do far more than execute ladder logic. Competitors are pairing PLCs with edge computing gateways, feeding real-time machine data into cloud-based analytics platforms. This integration enables condition-based monitoring, automated quality adjustments, and dynamic production scheduling capabilities that manual operations simply cannot match.

According to the Association for Advancing Automation, North American companies acquired 17,635 robots worth USD 1.094 billion in just the first half of 2025. These robots communicate through PLC-controlled networks, and the companies deploying them are reducing labor costs by 25–30% while simultaneously improving throughput consistency.

Industrial IoT Solutions Are Creating Data-Driven Advantages

71% of organizations already use AIoT for predictive maintenance. The ones going deep on AI are twice as likely to beat their ROI targets.

Industrial IoT solutions connect physical equipment to cloud and edge platforms, transforming raw sensor data into actionable operational insights that drive predictive maintenance, energy optimization, and real-time quality control.

Industrial IoT development services have moved from experimental pilot programs to enterprise-scale deployments. IDC research confirms that 71% of organizations now use AIoT (the convergence of AI and IoT) for predictive maintenance, making it the most widely adopted use case across industries. Organizations that deeply employ AI within their IoT ecosystems are twice as likely to report benefits that significantly exceed expectations, with 63% citing productivity and competitiveness gains.

The fastest path to measurable ROI from industrial IoT is predictive maintenance companies adopting it reduce maintenance costs by 25–30%, cut unplanned downtime by 35–50%, and typically achieve full cost recovery within 12 months.

The convergence of these IoT platforms with production monitoring systems is where competitors are extracting the most value. Real-time vibration, temperature, acoustic, and pressure sensors blanket production floors, streaming millisecond-level data to analytics platforms. This continuous monitoring allows companies to spot degradation patterns weeks before a failure event.

Predictive Maintenance in Manufacturing Explained

Predictive Maintenance: The Killer Application

Unplanned downtime burns $50B a year across manufacturing. Predictive maintenance trims 25-30% of that cost and prevents 35-50% of events.

The financial case is staggering. Industrial manufacturers lose approximately USD 50 billion annually to unplanned downtime, with median costs exceeding USD 125,000 per hour across industries (IoT Analytics). In semiconductor manufacturing, each hour of unexpected downtime costs over USD 1 million.

Competitors using IoT-driven predictive maintenance are reducing maintenance costs by 25–30% and cutting unplanned downtime by 35–50%. AI-driven analytics extend equipment life by 20–40%, deferring capital expenditures that would otherwise drain cash flow. In the chemical processing sector alone, predictive systems have reduced urgent maintenance work by 40%. Steel manufacturers report USD 1.5 million in annual savings. Power generation companies have documented USD 7.5 million in avoided failure costs through sensor-based early warning systems (IIOT World, 2026).

The practical first step in a manufacturer's AI journey is often predictive maintenance it delivers clear ROI while catalyzing the cultural shift toward data-driven operations that enables broader industrial AI solutions.

Digital Twin Software Is Rewriting the Rules of Manufacturing

92% of companies investing in digital twins report ROI above 10%. Half of them hit 20%+ returns within one to three years.

Digital twin software creates real-time virtual replicas of physical assets, production lines, or entire factories, enabling simulation, prediction, and optimization without disrupting actual operations.

The global digital twin market grew from USD 24.48 billion in 2025 to USD 33.97 billion in 2026 and is projected to reach USD 384.79 billion by 2034 at a 35.4% CAGR (Fortune Business Insights). Manufacturing is the dominant application sector and the fastest-growing category for digital twin adoption.

McKinsey research shows that digital twins cut development times by up to 50%, deliver a 20% improvement in consumer promise fulfillment, reduce labor costs by 10%, and increase revenue by 5%. According to a Hexagon survey of over 500 manufacturers, early digital twin adopters achieve approximately 15% cost reduction and 25% or greater operational efficiency gains within the first year.

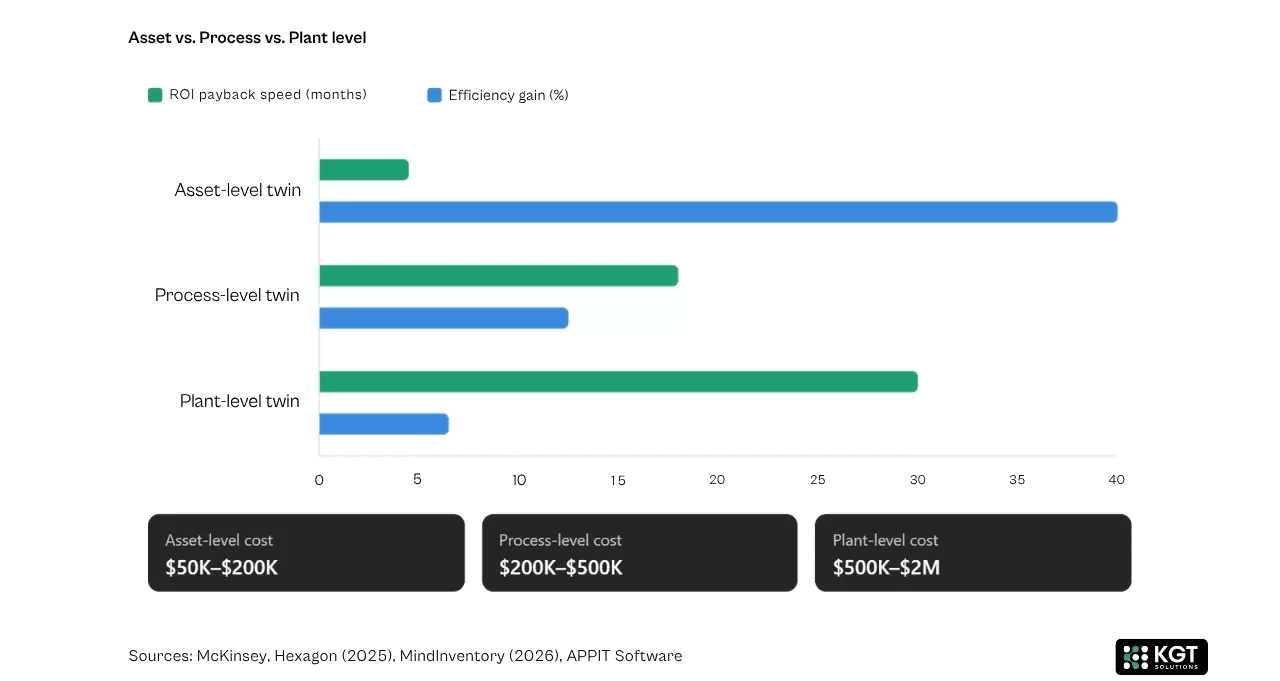

Competitors are deploying digital twins at three levels of maturity. Asset-level twins monitor 10–20 critical machines for predictive maintenance, typically costing USD 50,000–200,000 and delivering ROI in 3–6 months. Process-level twins simulate entire production lines and can improve throughput by 10–15%. Plant-level twins model the full factory - machines, material flow, energy systems, and workforce reducing total manufacturing costs by 5–8%. For a practical breakdown of how digital twins work in practice, including the data, simulation, and visualization layers.

A critical statistic: 92% of companies that have invested in digital twins report ROI above 10%, with half achieving returns of 20% or more within 12–36 months of deployment (MindInventory, 2026). Competitors who have moved past pilot stages are locking in pricing advantages, hitting ESG targets first, and attracting top engineering talent.

Why 2026 Is the Inflection Point

Digital twin patents jumped 600% between 2017 and 2025. Now 65% of manufacturing tech leaders say they are deploying this year.

Digital twin technology reached its mainstream inflection point in 2026 because pre-built models eliminated the cold-start problem, cloud costs fell enough for mid-market viability, and patent filings surged 600% from 2017–2025, signaling rapid technology maturation.

Three developments make 2026 the year digital twins go mainstream. First, pre-built models now ship with platforms for common manufacturing equipment, eliminating the "cold start" problem. Second, cloud infrastructure costs have fallen enough to make plant-level twins economically viable for mid-market manufacturers. Third, digital twin patent filings surged 600% from 2017 to 2025, with 2,451 applications filed in 2025 alone (PatSnap), signaling that the technology landscape is maturing rapidly.

According to Forrester research, 65% of manufacturing technology decision-makers plan to deploy digital twins to optimize operations, and 67% will prioritize the technology for full product lifecycle sustainability. Competitors already past the planning phase have a meaningful head start.

Warehouse Automation Is Reshaping Fulfillment Speed

80% of warehouses still run without automation. The ones that moved early? 250% ROI, with AMR payback under 24 months.

Warehouse automation uses robotics, AS/RS, conveyor networks, and AI-driven software to accelerate order fulfillment, reduce errors, and dramatically lower labor dependency in distribution operations.

The global warehouse automation market is valued at USD 29.98 billion in 2026 and is projected to reach USD 59.52 billion by 2030, growing at an 18.7% CAGR (Grand View Research). Despite this explosive growth, 80% of warehouses still operate without automated systems, meaning early movers are capturing disproportionate competitive advantage.

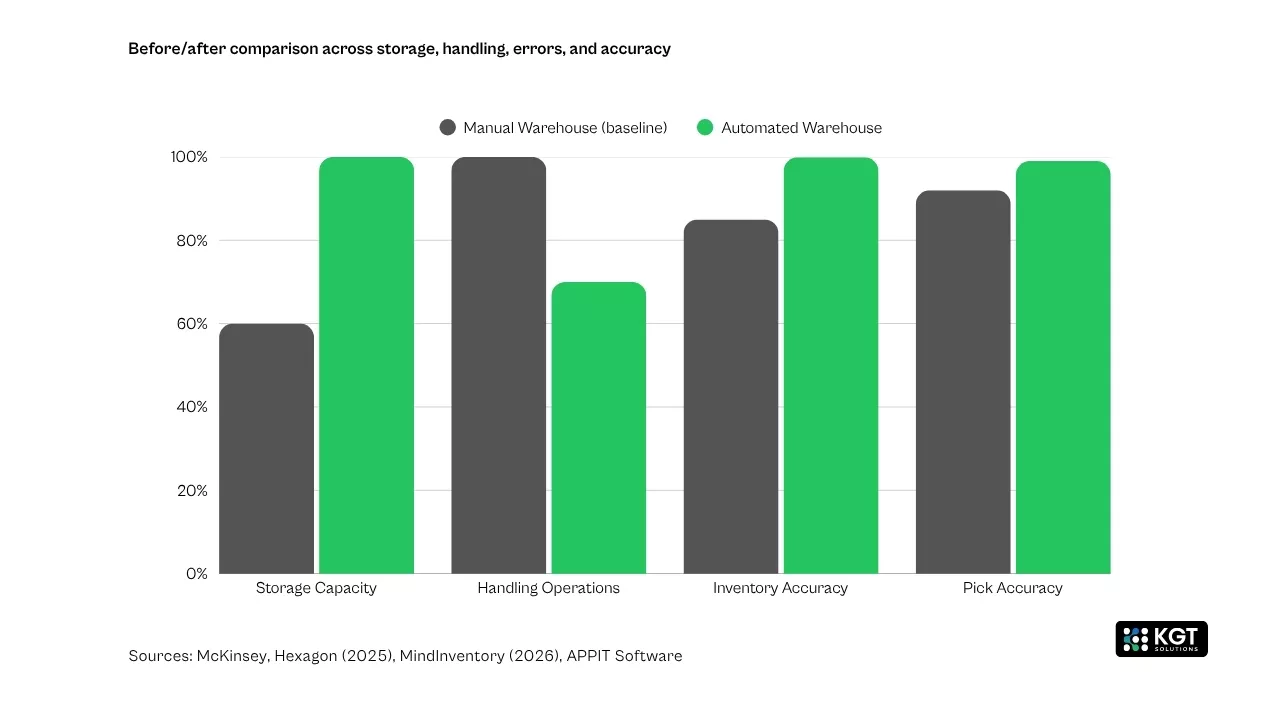

Data warehouse automation tools and warehouse management systems are the software backbone of this transformation. A modern WMS can deliver up to 40% more storage capacity, 30% fewer handling operations, and a 99% reduction in inventory errors. The WMS market alone was valued at USD 4.72 billion in 2025 and is projected to reach USD 21.23 billion by 2035 at a 16.23% CAGR (SNS Insider, 2026).

Autonomous Mobile Robots (AMRs) deliver payback in under 24 months and ROI above 250% in live deployments. These are the returns nobody talks about in standard CapEx proposals. Over 450,000 logistics robots were sold worldwide in 2025, a 500% increase from 75,000 in 2019. Automated storage and retrieval systems save up to 85% of storage space while cutting manual labor requirements by two-thirds and improving pick accuracy to approximately 99%.

Warehouse automation ROI is driven primarily by labor substitution with labor accounting for 50–70% of total warehousing costs and wages rising 7–9% annually, even modest automation deployments achieve payback within eight months.

Labor accounts for 50–70% of total warehousing budgets, and logistics wages climbed 7–9% year-over-year in 2024. This is the same labor crisis driving how automation fills the 2M manufacturing job gap across every sector Competitors deploying automated fulfillment systems are converting this cost pressure into a structural advantage documented deployments show eight-month payback periods when workers are shifted to value-added tasks rather than eliminated. Leading vendors now offer a broad catalog of industrial automation products - from AMRs and AS/RS units to conveyor networks and AI-driven sortation allowing companies to assemble solutions tailored to their specific throughput and SKU complexity requirements.

Robotic Process Automation (RPA) Services Extend Beyond the Factory Floor

RPA pays for itself fast: 100-200% ROI in the first year, slashing 30-80% of costs on repetitive processes across the operation.

Robotic process automation (RPA) services deploy software bots to handle repetitive, rule-based tasks across business operations from order processing and invoicing to compliance reporting and supply chain coordination.

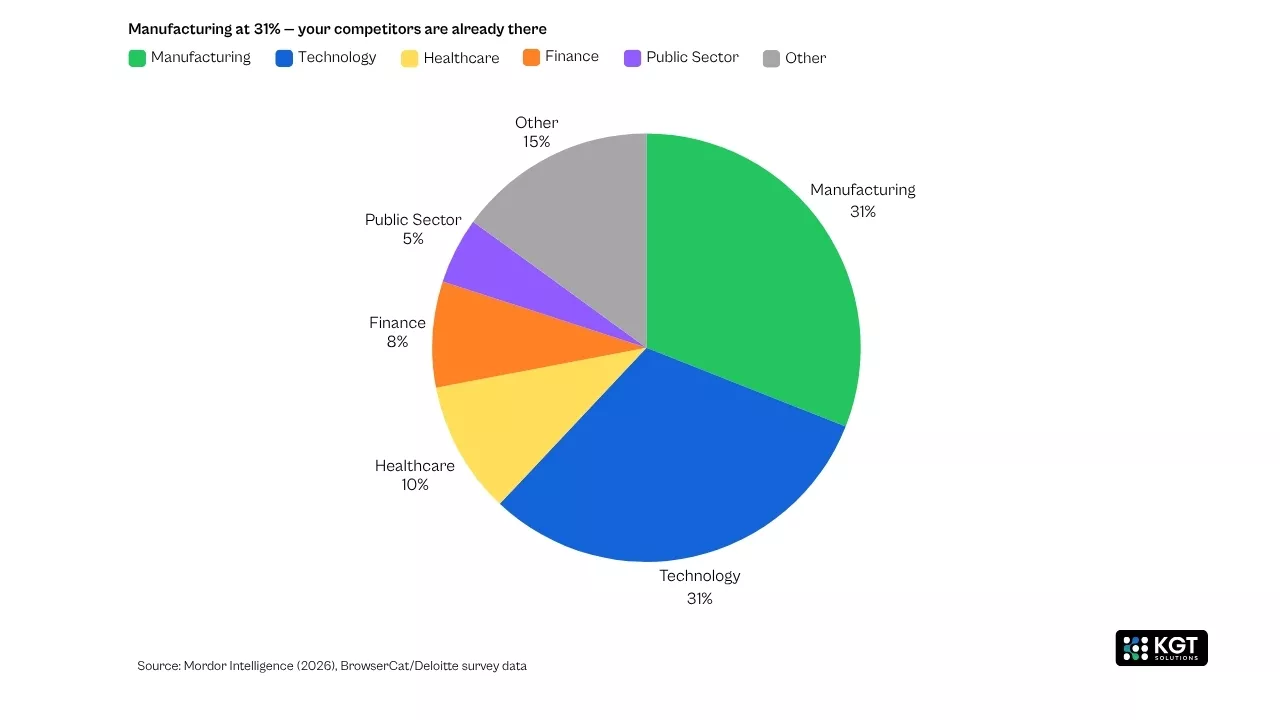

While industrial automation transforms the shop floor, robotic process automation RPA services are giving competitors an edge in the back office. The global RPA market was valued at USD 22.58 billion in 2025 and is projected to grow to USD 110.06 billion by 2034, at a 19.1% CAGR (Fortune Business Insights). Manufacturing leads RPA adoption at 30.68% of the market (Mordor Intelligence, 2026).

The ROI case is compelling. Most RPA projects generate 100–200% ROI in the first 12 months. For repetitive processes, automation reduces operational costs by 30–80% compared to manual handling. RPA bots run around the clock, boosting productivity 3–5x over manual processes and automating 70–80% of rules-based business tasks.

RPA creates the most value in manufacturing when connected to shop-floor IoT a sensor-triggered anomaly can automatically generate maintenance work orders, update ERP records, and order parts within seconds, eliminating information delays that cost hours in manual environments.

Competitors are connecting RPA with IoT platforms to create end-to-end automation chains. When a sensor on a production monitoring system detects an anomaly, an RPA bot can automatically generate a maintenance work order, update the ERP system, notify the relevant technician, and order replacement parts all within seconds. This integration eliminates the information delays that slow down manual operations and compounds the efficiency gains from both shop-floor and back-office automation.

Grupo Éxito, a major retailer, cut order-processing times by 75% after deploying enterprise-wide RPA that connects e-commerce front-ends with legacy ERP data (Mordor Intelligence). These kinds of results are replicable across any manufacturing or distribution operation with repetitive administrative workflows.

Industrial AI Solutions Compound Every Other Automation Investment

Layer AI analytics across your systems and you get 50% less unplanned downtime, 25% lower maintenance costs, and 20-40% longer asset life.

Industrial AI solutions apply machine learning, computer vision, and advanced analytics to industrial data, enabling autonomous decision-making, quality prediction, and continuous process optimization at speeds impossible for human operators.

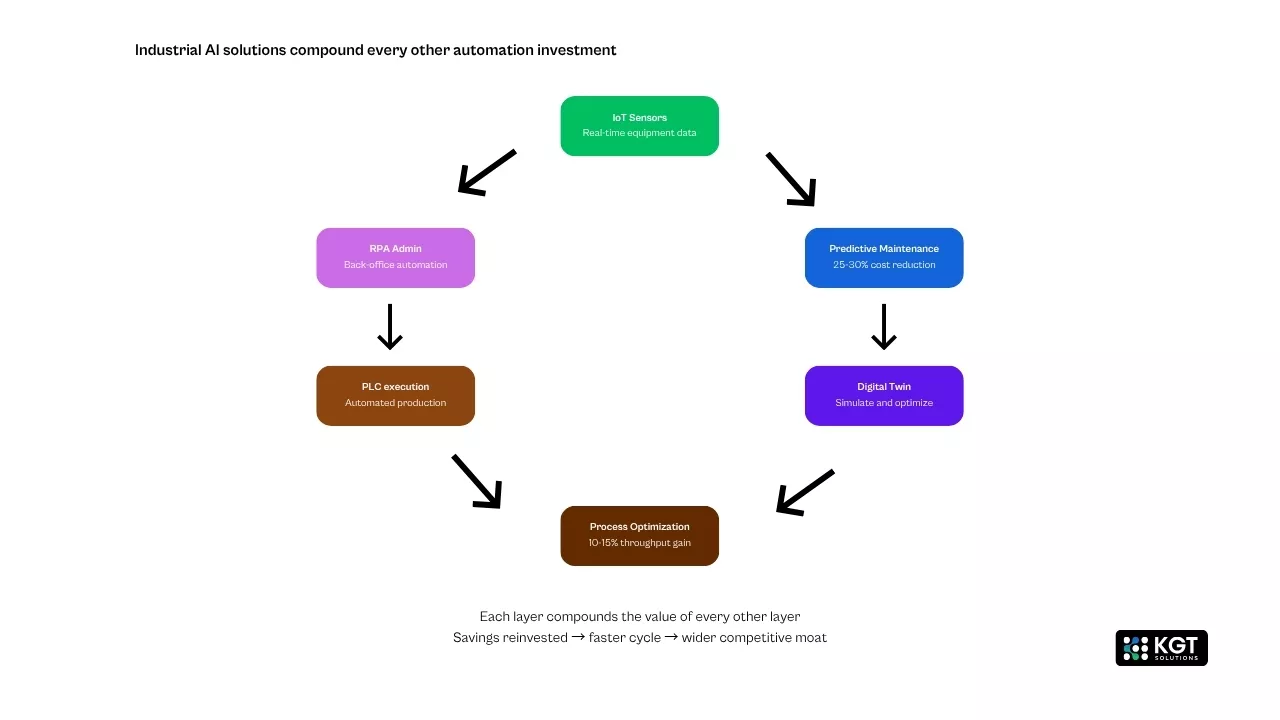

The real competitive threat is not any single automation technology it is the compounding effect when AI ties everything together. AI-powered predictive maintenance reduces downtime. That improved uptime feeds better data into digital twin software. The digital twin identifies process optimization opportunities. Those optimizations flow through PLC-controlled production lines. RPA automates the administrative workflows around each improvement. The result is a continuously learning, self-improving operation.

Fanuc partnered with NVIDIA in 2025 to develop AI-powered industrial robots that enhance autonomous smart factory automation. Yokogawa Electric Corporation collaborated with Shell to integrate AI robotics and machine vision for autonomous plant operations. These are not experimental projects they are production deployments by market leaders embedding AI into their core operations.

Organizations deploying AI-driven analytics to equipment data are cutting unplanned downtime by up to 50%, reducing maintenance costs by approximately 25%, and extending asset life by 20–40%. The companies that have moved first are using these savings to fund the next wave of investments, creating a compounding advantage that grows with every quarter.

Industrial AI solutions deliver the greatest competitive impact when they connect predictive maintenance, digital twins, PLC-controlled production, and RPA into a single learning system each layer compounds the value of the layers beneath it.

Production Monitoring Systems Enable Real-Time Decision Making

Production monitoring systems provide continuous, real-time visibility into equipment performance, output quality, and process efficiency, enabling operators and managers to make data-driven decisions instantly rather than waiting for end-of-shift reports.

Modern monitoring platforms integrate directly with control hardware and IoT sensor networks to create a unified operational picture. When paired with industrial PLC programming, these systems can trigger automated responses adjusting machine parameters, diverting defective products, or rebalancing production schedules without human intervention.

The SCADA segment within industrial automation is expected to witness the fastest CAGR through 2033, driven by increasing demand for real-time process visualization, remote asset monitoring, and centralized control across critical infrastructure. The integration of SCADA with cloud platforms and edge computing is enhancing analytics and decision-making capabilities (Grand View Research, 2026).

By 2025, nearly half of all enterprise data was processed at the edge rather than in the cloud, enabling sub-second anomaly detection and automated responses in time-critical manufacturing environments where milliseconds determine product quality.

The Monitoring Systems That Create Asymmetric Advantages

Competitors are extending monitoring beyond the factory floor. Surveillance system wireless deployments now cover entire facility perimeters, supply chain handoff points, and remote equipment installations. Tyre pressure monitoring systems in fleet operations connected to centralized dashboards help logistics companies reduce downtime and fuel costs simultaneously. Even a monitoring system for elderly care facilities is adopting the same IoT sensor and cloud analytics architecture that powers industrial automation demonstrating how the technology patterns proven in manufacturing are expanding across sectors.

The common thread is data-driven, continuous monitoring paired with automated response. Whether the use case is a production line, a warehouse, or a fleet of delivery vehicles, the competitive advantage flows from the same capability: seeing problems before they become expensive, and responding faster than competitors who rely on manual checks.

How to Close the Industrial Automation Gap

Find the 20% of assets causing 80% of your downtime. Put sensors on those first. Target 30% downtime reduction in six months.

To close an automation gap against competitors with a multi-year head start, begin with predictive maintenance on your highest-risk assets, build a scalable data infrastructure, and layer intelligence progressively from rules-based alerts through machine learning to full digital twin optimization.

If your competitors have a two- or three-year head start in automation, closing the gap requires a deliberate strategy. The playbook used by successful fast-followers shares several common elements.

Start with the 80/20 rule. Identify the 20% of assets responsible for 80% of your downtime risk or maintenance costs. Deploy IoT sensors and predictive maintenance on those critical machines first. Set concrete success metrics reducing unplanned downtime by 30% on a specific line, or cutting maintenance overtime by half on a specific process. Calculate your automation ROI in 90 days to build the business case that unlocks budget. Even a small-scale pilot on high-value targets delivers measurable ROI that builds organizational momentum.

Build your data infrastructure in parallel. Select a scalable data platform cloud-based data warehouses or IoT hubs to centrally collect and manage IIoT data from dozens or hundreds of machines in real time. Data warehouse automation tools streamline this process, ensuring that operational data flows into analytics platforms without manual ETL bottlenecks.

Invest in PLC connectivity. Ensure OPC UA or Modbus access to all critical machines. Modern automation platforms require minimum 3–6 months of historical data for statistical models, standardized machine IDs, consistent parameter naming, and time-synchronized data sources. Getting this foundation right determines whether your automation investments deliver results or stall in pilot purgatory.

Layer intelligence progressively. Start with condition monitoring and rules-based alerts. Graduate to machine learning–based anomaly detection. Then deploy digital twin software for simulation and optimization. Each layer compounds the value of the layers beneath it.

Finally, connect shop-floor automation with back-office RPA. The organizations seeing the largest competitive gains are those that have eliminated the information gaps between machines, maintenance teams, procurement, and finance.

The Compounding Cost of Inaction

Every quarter without industrial automation widens the gap between you and competitors who are already capturing 25–50% reductions in downtime, 15–30% ROI on digital twin investments, and 30–200% first-year returns on RPA deployments.

The industrial automation market employs approximately 1.6 million professionals worldwide (StartUs Insights, 2026) and is supported by over 26,200 companies globally. Innovation intensity remains high, with more than 54,200 patents filed by 24,500+ applicants. This is not a niche technology category it is the core operating system of modern manufacturing, and the competitors who have committed to it are pulling away.

The question is not whether to automate. The question is how quickly you can build the integrated architecture spanning control systems, IoT platforms, digital twins, automated warehouses, RPA, and AI that turns your operations into a compounding competitive advantage.

Frequently Asked Questions

What specific automation technologies give competitors the biggest advantage in manufacturing?

How much market share can a company lose by not investing in industrial automation?

What is the minimum automation investment needed to stay competitive in manufacturing?

How quickly can competitors scale their automation advantage over companies that delay?

Can small manufacturers compete with larger automated competitors?

Sources:

Persistence Market Research (2026). Industrial Automation Market Size & Forecast, 2026–2033.

Mordor Intelligence (2026). Industrial Automation Market Size, Share & Growth Report, 2026–2031.

Grand View Research (2025). Industrial Automation and Control Systems Market Report.

IoT Analytics (2024). Predictive Maintenance Market: 5 Highlights for 2024 and Beyond.

McKinsey & Company. Predictive Maintenance: Transforming Industrial Operations; Supply Chain Digital Twins Research.

Fortune Business Insights (2026). Digital Twin Market Size, Share & Growth Report, 2026–2034.

Hexagon (2025). 2025 Digital Twin Statistics.

MindInventory (2026). Digital Twin Statistics 2026: Market Size, Adoption Trends, ROI, and Real-World Impact.

PatSnap (2026). Digital Twin Tech Landscape for Manufacturing 2026.

Grand View Research (2025). Warehouse Automation Market Size and Share Report, 2030.

SNS Insider (2026). Warehouse Management System Market Size Report.

SellersCommerce (2026). Warehouse Automation Statistics 2026.

Fortune Business Insights (2026). Robotic Process Automation (RPA) Market Size Report, 2025–2034.

Mordor Intelligence (2026). Robotic Process Automation Market Size & Forecast, 2025–2031.

IDC Research. AIoT Predictive Maintenance Adoption Study.

International Trade Administration (ITA). Industrial Robot Density and Productivity Correlation Study.

Association for Advancing Automation. North American Robotics Acquisition Data, H1 2025.

StartUs Insights (2026). Industrial Automation Report 2026.

NIST AMS 100-61 (2024). The Economics of Digital Twins: Costs, Benefits, and Economic Decision Making.

WorkTrek (2026). 8 Trends Shaping the Future of Predictive Maintenance.

IIOT World (2026). Predictive Maintenance: Cutting Costs & Downtime Smartly.

Industrial Autonomous Floor

Newsletter

Actionable insights on industrial AI, automation, and smart operations built for safe, secure, and compliant real-world environments.